Direct Deposit For Small Businesses: A Guide

by

byTry When I Work for free

Direct deposit for small businesses is easier than you might expect. Here are the key things you need to know:

- Direct deposit isn’t just for big companies

- Direct deposit offers convenience for your staff

- You can save time and money by setting up direct deposit

- Setting up automated deposits is easier than you might expect

- When I Work can simplify your payrolling and direct deposit workflows

Thanks to modern tech tools, setting up direct deposit for small businesses isn’t just attainable—it’s pretty easy! You can pay your employees in a way that is more convenient for everyone. Explore the ins and outs of direct deposit for small businesses.

- What is direct deposit?

- Direct deposit vs other payment methods

- Benefits of direct deposit for small businesses

- Challenges of direct deposit for small businesses

- How to set up direct deposit for your small business

- How to make direct deposit easier

- Streamline your small business payroll management with When I Work

- Direct deposit for small businesses FAQs

What is direct deposit?

Direct deposit is an electronic funds transfer that sends money from one bank account to another. In the employer-employee context, it means sending pay directly to your employee’s bank account. They won’t have to cash a physical check but will instead have immediate access to their money on payday.

Technically speaking, a direct deposit is an automated clearing house (ACH) payment. ACH is the U.S. financial network that oversees account-to-account transactions. When you set up direct deposit for a small business, you are automating the process of paying your employees.

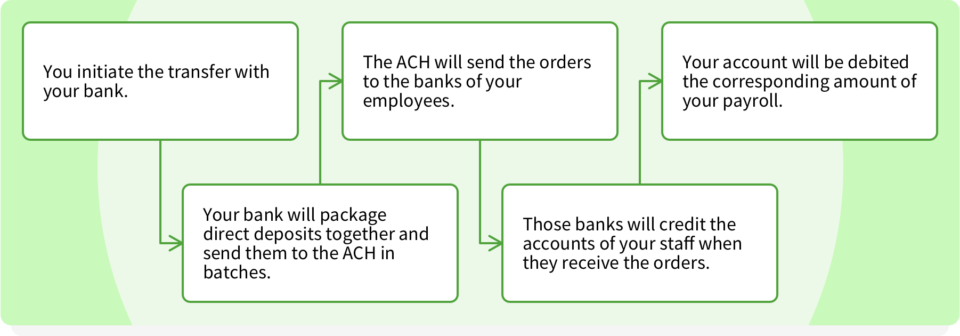

How direct deposit for small businesses works

Here’s how small business direct deposit works:

- You initiate the transfer with your bank.

- Your bank will package direct deposits together (e.g., payroll transfers for all your staff) and send them to the ACH in batches.

- The ACH will send the orders to the banks of your employees.

- Those banks will credit the accounts of your staff when they receive the orders.

- Your account will be debited the corresponding amount of your payroll.

Sounds easy enough, right? We think so, too!

How much it costs

The costs of direct deposit for small businesses will vary based on factors like how many employees you have and which institution you bank with. Most banks typically charge a set-up fee to initiate direct deposits. This fee is usually a few hundred dollars.

Some banks may also charge a recurring direct deposit fee. Check with your financial institution to obtain specific information about direct deposit costs.

Is direct deposit only for larger businesses?

No, direct deposit is a convenient option for businesses of all sizes. Using direct deposit to streamline payrolling is one of our favorite tips for making small businesses more efficient and productive.

Is direct deposit legally required?

No, direct deposit isn’t legally required by federal law, but employers do have the right to require it for payroll processing, as long as employees can choose their own banks. As always, be sure to check your state and local labor laws for any specific statutes that may affect your specific business.

Direct deposit vs other payment methods

Here’s a quick, at-a-glance comparison table to help you see how direct deposit compares to other payment methods:

| Direct deposit | Paper checks | Payroll cards | |

| Cost | Initial setup fee with low recurring cost, eliminates material expenses (paper/postage) | High material and labor costs | Low to moderate costs, may involve account setup or provider transaction fees |

| Speed | Immediate access on payday, automated processing requires setup several days in advance | Slower, requires physical deliver, employees must take checks to the bank to cash them | Immediate access on payday, funds are electronically loaded onto the card |

| Security | Highly-secure ACH transfer network, eliminates risk of lost/stolen/misdelivered checks | Low security, higher risk of theft/loss/administrative error | High security, encrypted card data, though physical cards can still be lost |

| Employee preference | Very high, supports financial wellness, eliminates travel time to bank, often features early deposit | Low, inconvenient for the modern workforce, requires physical cashing or can result in mobile deposit holds | Moderate to high, good for unbanked employees, card fees can be a drawback |

Benefits of direct deposit for small businesses

Setting up direct deposit for small businesses will improve your payroll management capabilities and help you:

Save time and money

Investing in direct deposit can save you materials costs, as you won’t have to issue physical checks. You can reduce the need for overtime, too. Think about it this way. You and your payroll staff can spend less time issuing checks and verifying gross wages, reducing manual entry and human error.

This is especially important when calculating and handling employment and payroll taxes. Instead, you can use direct deposits and payrolling software to automate these processes, saving you on labor costs.

Minimize cash flow errors

Direct deposit can minimize cash flow errors by ensuring that all payroll and costs are promptly deducted from your account. Your account will automatically be debited when the ACH network processes payroll. This means you will have a more accurate view of your available cash.

Transfer funds securely

The ACH system is secure, meaning your employees will enjoy peace of mind knowing that their pay is going to the right place. You won’t have to worry about issues like an employee accidentally grabbing the wrong check or an administrative staff member putting a check in someone else’s box.

Reduce waste

You’ll drastically reduce paper waste by transitioning from checks to direct deposit. Depending on the size of your business, you may be able to eliminate hundreds of pieces of paper from your annual waste production.

Support employee financial wellness

Direct deposit promotes employee financial wellness by giving them immediate access to their funds on payday. They will no longer have to rush to the bank after work. Some banks even offer early deposit options, meaning employees can gain access to their wages one or two days early.

See how When I Work can help you simplify payroll when you add a payroll integration to save more time! Learn more about our available integrations and see how you can simplify scheduling and payroll for your team.

Challenges of direct deposit for small businesses

Setting up direct deposit does pose a few challenges, including the following:

Difficulty in stopping payments if you discover an error

If you discover an error, it will be difficult to stop the ACH payment from processing. Recalling the funds can be tough, too. Therefore, it’s best to implement automated systems that minimize the need for human input.

Time-sensitivity

You must have all payroll information calculated several days before employees are to be paid. This is because the ACH system will take a couple of days to process your requests.

Risk for overdraft fees

You could incur huge overdraft fees if your business account does not have enough funds to cover ACH transactions. Make sure to familiarize yourself with your financial institution’s fee schedule before setting up direct deposits.

Data security concerns

Some employees may be concerned about the security of their data. This is understandable, as direct deposits involve the sending of sensitive data like account and routing numbers as well as personal identifying information.

How to set up direct deposit for your small business

Setting up direct deposit for small businesses is pretty simple. Just follow these six steps.

1. Pick a provider

Decide which institution is going to handle your direct deposits. You can work directly with your bank or use payroll software with direct deposit capabilities. The latter approach gives you better insights into payroll costs. However, not all payrolling software is created equal.

When exploring payroll software options, find an all-in-one tool like When I Work. The platform offers everything from employee scheduling, time clock tools, integrations, and more.

Related read: When I Work Vs Connecteam (2026): Is All-In-One Slowing You Down?

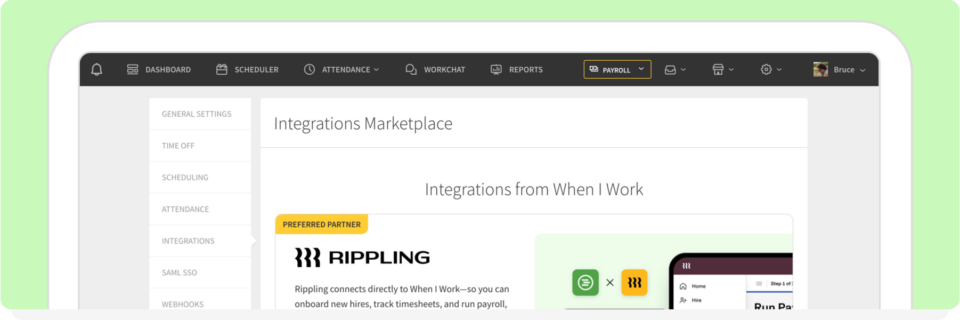

When I Work preferred payroll partner

Make payroll simple with our preferred partner Rippling, an all-in-one platform for payroll, benefits, and compliance. Together, When I Work and Rippling help you save hours every week while reducing errors, staying compliant, and getting your team paid on time.

2. Initiate the process

After you’ve decided on a provider, you’ll need to set up the process. Carefully review all ACH terms and conditions, even if you are going through a software platform. Be especially mindful of any fees or hidden expenses.

3. Collect employee information

Next, you’ll have to gather employee information to set up your direct deposits. At a minimum, you’ll need the following:

- Bank account number

- Routing number

- Bank’s name

- Account type (checking or savings)

Your employees will also have to sign an authorization form to give you permission to transfer the funds.

4. Enter the data into your system

Now, you can add the employee information to your payrolling software. Some systems allow your employees to add information themselves. If you go this route, make sure to verify each person’s data. Otherwise, they may experience pay delays.

5. Create a payroll schedule

Create a payroll schedule that aligns with your preferred pay intervals. The most common options involve weekly and biweekly payments.

Keep in mind that it can take 7-10 business days for your direct deposit workflows to go live. If the current pay period is ending, you may want to wait until the next cycle to start the direct deposits.

6. Run payroll

Finally, you can run your payroll. If you implemented full-service payrolling software, this stage should be quick and easy. Keep a close eye on everything to ensure that the new system goes off without a hitch and your employees get their paychecks on time.

How to make direct deposit easier

Modern payroll software is loaded with features designed to make payroll management quick and easy. You can use payroll software to implement automated payroll calculations, track employee hours, and hold everyone accountable.

That said, not all payroll software is created equal. It’s vital that you choose the right platform to support your direct deposit workflows.

Streamline your small business payroll management with When I Work

When I Work includes a time clock feature, scheduling capabilities, and automation capabilities, which yield significant time and cost savings.

When I Work also integrates seamlessly with payroll providers to save you even more time. Our payroll integrations, especially the one to our preferred partner,Rippling, help you connect scheduling and payroll automation in one streamlined workflow, so you can focus on running your business, instead of reconciling timesheets.

Ready to learn more about the benefits of When I Work? Sign up for a free trial today!

Direct deposit for small businesses FAQs

Can a small business set up direct deposit?

Yes! Direct deposit payroll is an efficient and convenient option for businesses of all sizes. Small businesses can easily set up direct deposit for employees to give them immediate access to their funds on payday.

How much does direct deposit cost for a small business?

Costs vary based on your bank and the size of your staff. Most banks charge a setup fee and some require recurring transaction fees for ACH direcct deposit. You should also be sure to keep an eye on your account balance to avoid high overdraft fees.

How hard is it for a company to do direct deposit?

It’s simple, especially when you use full-service payroll software. You just choose a provider, collect employee bank details and signed authorization forms, put the data into your system, create a schedule, and run your payroll.

Is there a downside to direct deposit?

The main downsides are strict time-sensitivity for processing and the extreme difficulty in stopping or recalling mistaken payments. You can face risks of overdraft fees if funds are low, and occasional employee data concerns.