The 10 Biggest Tax Mistakes Small Business Owners Risk Making

by

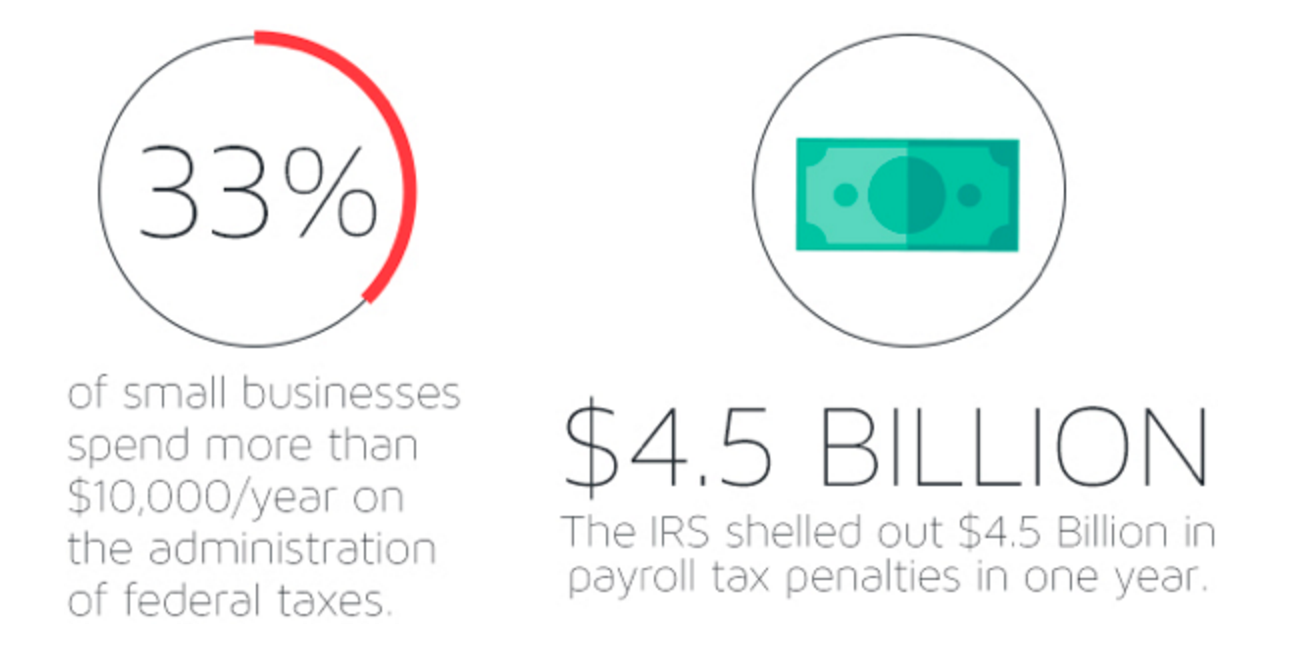

byYour business is your livelihood and you do everything you can to put best practices in place. But, businesses are run by humans and we are all capable of making mistakes. Especially when, like many small business owners, you’re wearing many hats each and every day.

Source: Wasp Barcode Technologies, 2015

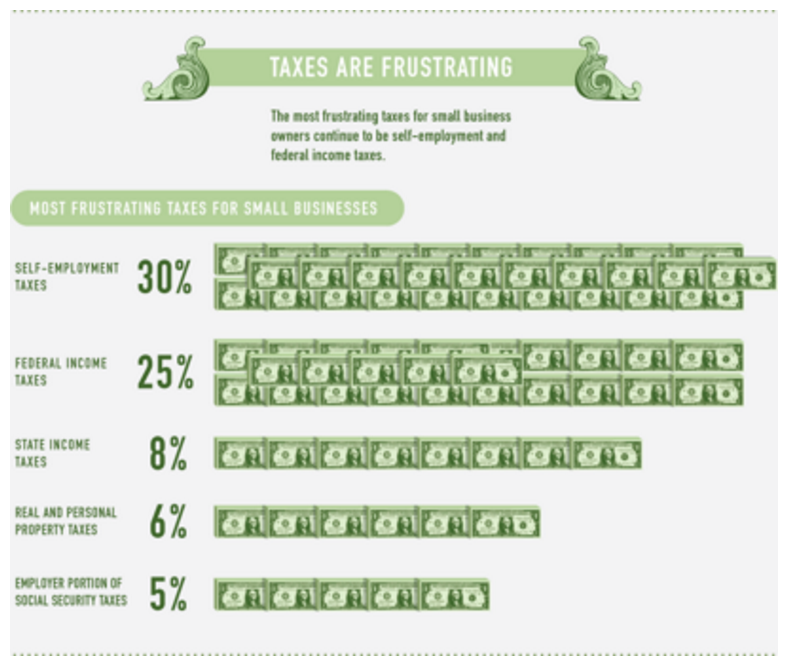

It’s Not Just You, No One Likes Doing Taxes

Tax is only a three-letter word, but it more than makes up for it by the number of four-letter words it generates as you try to figure them out and follow the rules.

Source: Intuit QuickBooks Blog

Learn From Those Who Have Gone Before You

There’s no escaping it — taxes are a part of doing business. But, by reading this post, you can stop yourself from falling victim to any of these top 10 small business tax blunders:

1. Mixing Business and Personal Finances

You know how mixing business and pleasure never really works out in the movies or on TV? It’s not such a good idea in the business world either.

According to small business funding app Fundbox: “If your business is a corporation, it’s considered a separate entity and finances must be completely separate to maintain the corporate shield that protects your personal assets. If you have structured your business as a sole proprietorship, the business is not a separate entity: You are entitled to all its profits and are also responsible for all of its debts, losses and liabilities. Still, business and personal finances should be separated because, in the event of an audit, the burden of proof is on you to prove your business expenses and income.”

2. Not Understanding Payroll and Employer Taxes

If only issuing a paycheck were as simple as writing a check. We’ll let you dream, just for one second. Ok, back to reality. Nothing operates in a vacuum and income must be properly reported to federal, state and local tax authorities as part of a process for contributing to social benefit programs and paying income taxes. The best way to make sure you’re reporting things correctly and saving the appropriate labor records? Use an employee scheduling software. When I Work offers a free employee scheduling app to track hours and overtime properly.

Source: Wasp Barcode Technologies, 2015

Federal and state payroll taxes are broken down into withholding amounts and employer-paid taxes:

- Withholding amounts include money that is deducted from a worker’s wages to pay for income tax, social security and Medicare (also known as FICA taxes). These amounts are deducted during each payroll then remitted on a regular basis to the proper tax authority by the employer. The schedule you follow depends on a number of variables.

- Employer-paid taxes, such as federal (FUTA) and state unemployment insurance (SUTA), are taxes that are paid entirely by the employer. Employers must contribute a matching amount of social security and Medicare (the same as what’s withheld from the employee’s check) and they are also responsible for reporting and remitting all of these amounts on a quarterly basis. (One perk — these expenses can be deducted from your business taxes.)

What happens if you make a mistake with your payroll and employer taxes? The Internal Revenue Service (IRS) has become less forgiving of small businesses that get their payroll taxes wrong and is more willing to issue fines, perform audits and, in certain cases, instigate criminal investigations.

3. Classifying Contractors as Employees (or Vice Versa)

Tax-wise, the biggest difference is that you don’t have to deduct any withholding amounts or pay any employer taxes for a worker who is legitimately an independent contractor (a self-employed person you contract for services who manages their own withholding and tax amounts and does not receive benefits). But, if you get this wrong, it means you’ve had it incorrect for every paycheck you’ve issued and you can be subject to fines along with the headache of untangling this mess. Misclassifying employees will also impact the deductions you claim on your business taxes, as the costs of contract labor are deductible as are employer-paid payroll taxes.

4. Claiming Too Many Expenses

CPA Practice Advisor writes, “Whether it’s for business travel, meals and entertainment, printing supplies, or other usually legitimate deductions, the IRS computers are good at looking at what similar small businesses in an industry type spend on similar expenses.”

The three most reviewed items are:

- The home office deduction

- Car expenses

- Travel and entertainment expenses

In addition to having data on average spending patterns, the IRS also requires proof that the expense was really a legitimate business expense and there are limits to how much you can claim for certain items. Substantiating a claim is a matter of having the appropriate documentation and filing for the right amount requires knowledge of the current tax codes. This is where working with the right tax professional can make all the difference.

5. Missing Out On Valid Deductions

While claiming too many expenses can raise a flag with the IRS, missing out on tax deductions you’re entitled to only punishes you and your business. Some of the deductions that small businesses often miss out on include:

- Startup costs — You can claim up to $5,000 the first year and equal amounts over the following 15 years for expenses related to getting your business off the ground.

- Interest on personal loans and credit cards — If you can verify that it was used for business purposes.

- Business services — Anything from PayPal transfers to Internet costs.

- Continuing education — If it’s related to your business.

- Inventory — You may deduct the costs of unpaid goods (but not services).

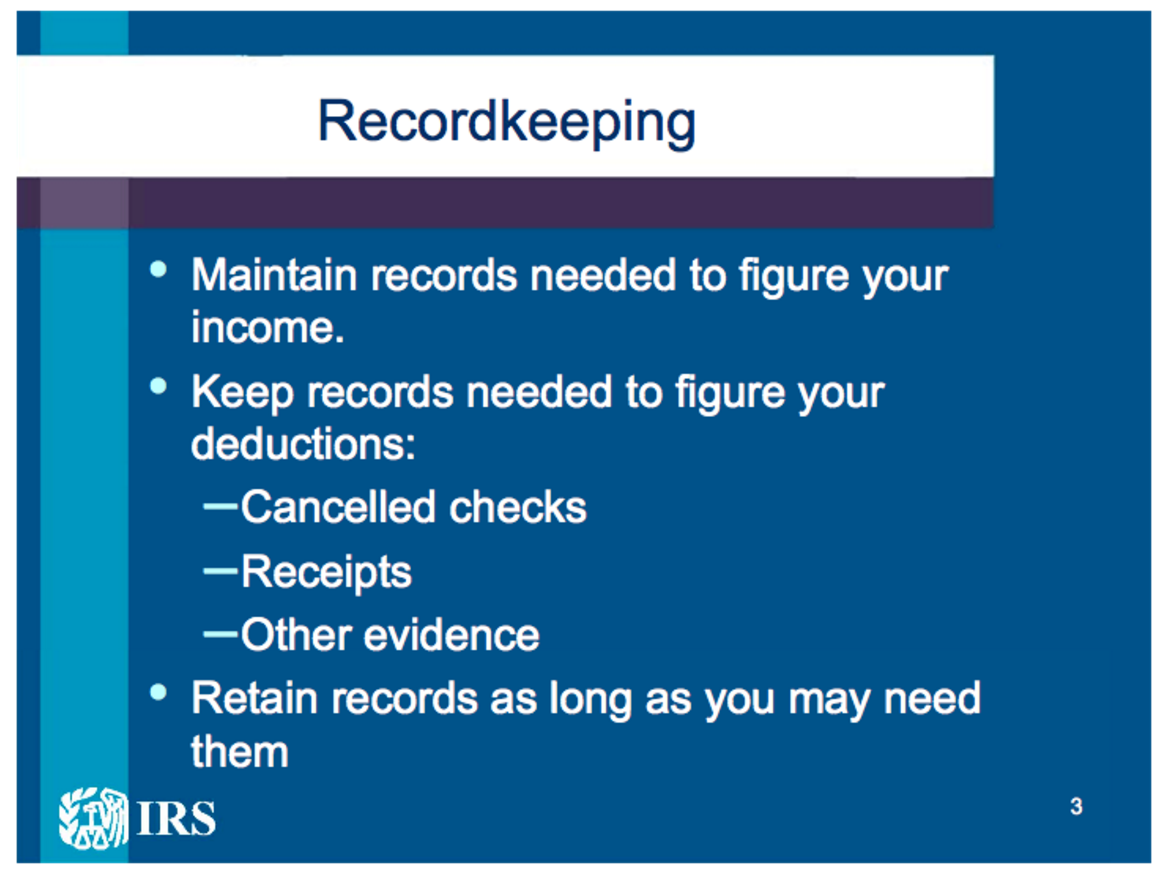

6. Poor Recordkeeping

Effectively documenting expenses and deductions requires a proper recordkeeping process. While you may strive to become paperless, going digital doesn’t mean ditching hard copies, especially if you’re ever audited. Note: The IRS recommendations vary depending on the kind of receipts filed.

Source: SlideShare from IRS Webinar

CPA firm delucia + co also recommends that small businesses reconcile their accounting statements on a regular basis. “Not reconciling statements — or not reconciling in a timely manner — keeps possible mistakes on your account past a time when they can easily be resolved. Negative results of failing to reconcile statements could include paying more than you expect for goods or services, paying bank or finance fees you didn’t agree to or bouncing checks due to mistakes in company checking accounts.”

Needless to say, the effects of not regularly reconciling your statements can snowball into your tax filings by causing you to submit the wrong amounts or miss deadlines all together.

7. Choosing the Wrong Legal Entity

When you first hang out your shingle as a small business or startup, it’s common to establish yourself as a sole proprietor or partnership. Although, as you grow, you may wind up paying too much in self-employed taxes and you could instead opt to structure yourself as a corporation.

Whether you’re a C Corporation, S Corporation or LLC that is taxed like an S Corporation, each one has specific tax implications. In her blog post, How To: Legally Structure Your Startup, Nellie Akalp, CEO & Co-Founder of CorpNet, provides the following example, “If I own 80% of an LLC, my share of the tax burden doesn’t necessarily have to be 80% of the taxable income. But if I own 80% of an S-Corp and that company makes $100,000 in taxable income, I will be taxed on $80,000 of income, even if I never withdrew a cent from the corporate bank account.” Meanwhile C Corps are taxed separately according to specific tax brackets.

The corporate structure you choose is a matter of what’s best for your business. It’s also a decision that affects the ways in which your taxes should be filed. Getting it wrong could mean a long and painful road to recovery.

8. Filing Late or Not Filing at All

If the deadline sneaks by you or you’re waiting for that one deal to close, it’s better to file late than not at all. Just like your mom always could — the IRS can see you even if you try to pretend it can’t. They also tend to get more and more agitated the longer you play this game. Any penalties you accrue by filing late or failing to file at all will continue to compound until you resolve the issue.

The IRS advises that you should, “File all tax returns that are due, regardless of whether or not you can pay in full.” If you are unable to pay the full amount, installment plans are available.

Get a head-start on next tax time with PaySimple’s Quick-and-Dirty Guide to Preparing Your Business for Tax Time.

9. Working With the Wrong “Expert”

Writing for the American Express OPEN Forum blog, Barbara Weltman, President and Founder, Big Ideas for Small Business, Inc. notes, “Don’t use anyone who suggests that you hide income or take write-offs you know you aren’t entitled to — this is a tip-off that the preparer is shady. If the IRS catches the preparer, all the preparer’s clients may come under audit. And, by not using a good preparer, you may miss out on write-offs you’re rightfully entitled to.”

Then there’s the fact that the IRS holds the business owner responsible for tax errors, regardless of who completed the filing. To help evaluate tax experts, try these tips for choosing a qualified professional to prepare your taxes.

Source: SlideShare from IRS Webinar

10. Not Using the Right Tools

The IRS cites poor record keeping and the failure to report all taxable income as the two biggest pitfalls for small business. The root of all evil (or many tendrils of pain and uncertainty) is maintaining proper documentation and ensuring that you comply with all applicable tax regulations.

Writing for the Intuit QuickBooks blog in a post titled, 10 Common Accounting Mistakes Small Business Make, author John Rampton states, “Accounting is not just a tool for entering financial data in order to fulfill state and federal tax regulations or to tell you how much money is in the bank. Instead, accounting is a powerful mechanism that provides answers to questions related to how a business owner’s strategic decisions are working or not working.”

The Young Entrepreneur Council (YEC) advises that startups choose a software (accounting, expense, productivity, etc.) that will not only fit them today, but will also suit their needs five years from now.

Choosing payroll software that suits your needs goes hand in hand with picking the proper accounting software. The right payroll provider will simplify the entire process. It will also help keep you in compliance with remitting and reporting your payroll taxes along with other key documentation. Plus, really who writes paper checks anymore?

One final recommendation: Make proactiveness your new best friend. Put the right tools and processes in place and do your best to keep yourself informed. Below is a list of tools available from the IRS. If you don’t have time to review them, at the very least make sure that the person doing your taxes knows what they are and how to use them.